We have a ValueLine subscription and after some first-hand experience with it, we can attest how practical and useful the reports are. The company was founded in 1931 and has been a great resource used by many investors throughout the years. You have probably heard your favorite value investor mentioning it as a great way to start the research process and to have a quick glance at the company’s history.

In this post we are compiling how Li Lu went about reading Value Line to invest in Timberland in 1998 (now part of VF Corporation) at a Columbia Business School lecture. We also share some personal tips we’ve gathered from personal experience to speed up your learning.

We love this lecture because it provides a window at how a lecture at Columbia goes and how the mind of a great investor works. Moreover, Li Lu’s attitude at the lecture is great: it challenges students, brings honesty to the table and demands quick wit and commong sense. He highlights that real value investors 1) thrive when being alone and having the chance to make their own decisions; 2) spend most of the time doing the job of an academic researcher with insatiable curiosity, wanting to know how everything works (businesses, politics, humanity, poetry). He also discussed how he, at the beginning of his carreer, read the whole ValueLine guide (which has about 3,500 companies), in the same way as Buffett did with Moody’s manuals.

The structure of a ValueLine report is simple. We have segmented one in three parts.

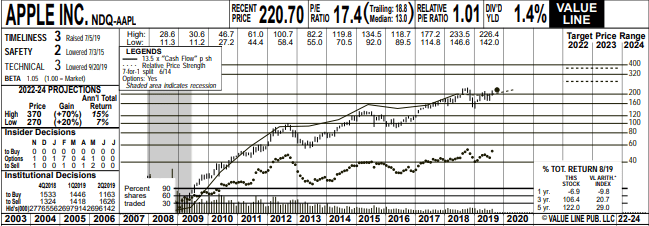

The first one has mostly descriptive tools, recent price, PE ratio, dividend yield and a graph with the price. On the left side we see the price projections made by the VL team and where the company ranks based on their Timeliness, Safety and Technical classification system, with 1 being the best score and 5 the worst.

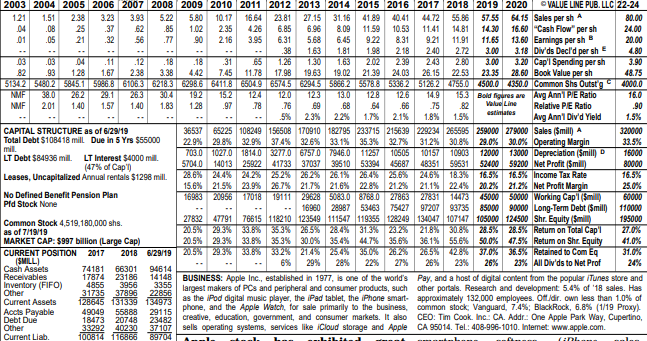

The second part is where we can take a look at the historical data of the company at a quick glance. Each company has different metrics depending on its industry, for example there are some differences between an insurance company and a tech one and the fields available for each. However, the reports are mostly homogeneous and easy to compare between sector players. Important to note that on the left hand side we have market cap, number of shares and a snapshot of the capital structure. Moreover, in the small business description at the bottom, we have a summary of ownership (both from insiders and external partners). In our view, this is the main playground of any investor, as like Li Lu shows, this is where one can discard or become very interested in a company via simple mental calculations.

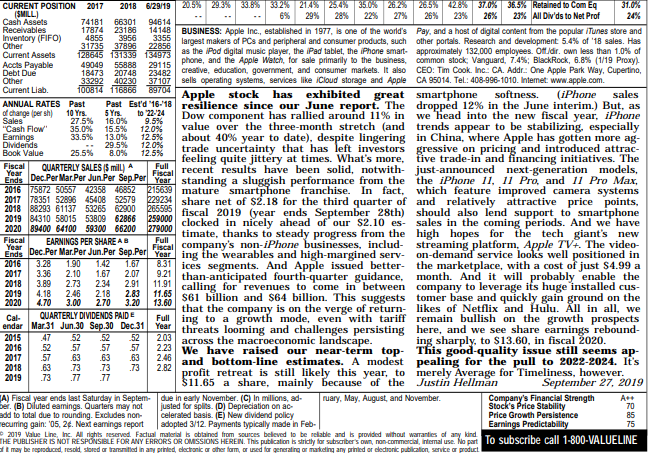

The third part has a write-up from the analyst, a brief score for the company’s financial strength, price stability, price growth performance and earnings predictability.

After getting acquainted with a ValueLine report, we can understand and follow through Li Lu’s tips. Here are his main highlights for a VL report:

- What is the first thing that jumps to you? Look at the valuation (if not good, do not go beyond. Note the case that Li Lu exposed applies to the fallen angels category.

- In this case the company was below book value, but what is in the book value? In this particular case, a big part of the working capital is inventory. Moreover, this report was available at the end of Q3 and in the retail segment, therefore we would need to check for seasonality. It may be that Q4 is strong and a good portion of it will be quickly converted into cash. Check also fixed assets and add all these to evaluate downside protection.

- Check the operating earnings and pre-tax earnings and compare vs. unleveraged capital needed by the business. Have the ability to calculate both these quickly. (Liquid assets + fixed assets = invested capital, a good proxy similar to the official Fixed assets + non-cash working capital). This should be done in a quick glance, something of 5 seconds.

- If the first two points are satisfactory, understand the reason behind the cheapness of the stock. Check how many analysts are covering the company.

- Check if the business has been steadily profitable and growing.

- Check the ownership structure. Check how much they own and how much they can vote.

- Understand the problems: in this case there were some lawsuits against the company.

- If after all these filters the idea is still interesting: you download every single piece of information and go through them all. This is done via the natural curiosity a true investor has.

Complement these Li Lu’s tips with Mr. Buffett’s take on the 11 characteristics of wonderful businesses.

As we can see, ValueLine provides a one-stop shop to answer many of the first questions that come to mind when looking at a business for the first time. Naturally, we recommend following along Li Lu’s comments on how to perform the analysis and size up the position. Needless to say, Li Lu’s fund went on to grab a shitload of stock (his words), which as he describes, went up close to 7x in the coming years. Li Lu closes that segment on the conversation suggesting that one should be able to go through an interesting company in less than 5 minutes in ValueLine, before going on and reading more data. Based on our experience, we would say that after reading many reports, it is feasible to do this quickly indeed. However, we also highlight that one starts becoming (as Buffett would sometimes call Munger) The Abominable No Man, as many companies that do not meet the requirements are discarded soon enough.

To close this article, we would like to pass on some personal tips we’ve encountered from reading VL reports.

- Go over market cap vs debt and WC: An interesting category (still, at least for us) is to check for potential net-nets. A quick glance into these lines would give an idea to figure out if this is feasible.

- Check ROE / ROIC (stability): For compounders, while a high ROIC/ROE is important, it is vital to see the historical trend. Generally, a stable figure should speak of an important competitive advantage.

- Check profit margin: in line with the previous bullet, it is vital to understand how a company is doing in terms of profits and understand how sustainable the trend is. If we see volatile trends, it will become very important to understand if there are any accounting tricks and/or capital structure changes.

- Check sales trend: While profits are easily manipulated in the short-term, this is not the case with sales. Always check that people are buying the company’s products/services at good growth rates.

- Check number of shares: It could be possible that most of the increase in profits stems from financial engineering. Checking that the number of shares diminishes is not bad on its own, but should be accompanied by the checks we described before.

- Check ownership by management (skin in the game): While many managers are paid via stock options, knowing that they are with us as investors for the long haul is important. VL includes this data in the business description, including main shareholders.

Finally, we encourage you to read our article on What is a value trap and how to avoid it, so you are well equipped to start your research!